If you use a vehicle for business purposes in Canada, the Canada Revenue Agency (CRA) allows you to deduct the business-use portion of your vehicle expenses from your taxable income. For the 2025 tax year, understanding exactly what qualifies, how to track it, and what limits apply can mean hundreds — or even thousands — of dollars in legitimate tax savings. Whether you are self-employed or an employee who uses a personal vehicle for work, this guide covers everything you need to know about vehicle expense deductions, logbook requirements, Capital Cost Allowance (CCA), and operating costs.

Not everyone who drives to work can claim vehicle expenses. The CRA distinguishes between commuting (which is never deductible) and genuine business travel. Here is who qualifies:

If you operate a sole proprietorship, partnership, or are an incorporated business owner who pays themselves employment income, you can deduct the business-use portion of vehicle expenses on your T1 personal return (Form T2125) or corporate return. This includes freelancers, contractors, tradespeople, real estate agents, and consultants.

Employees can claim vehicle expenses only if they meet all three of the following conditions:

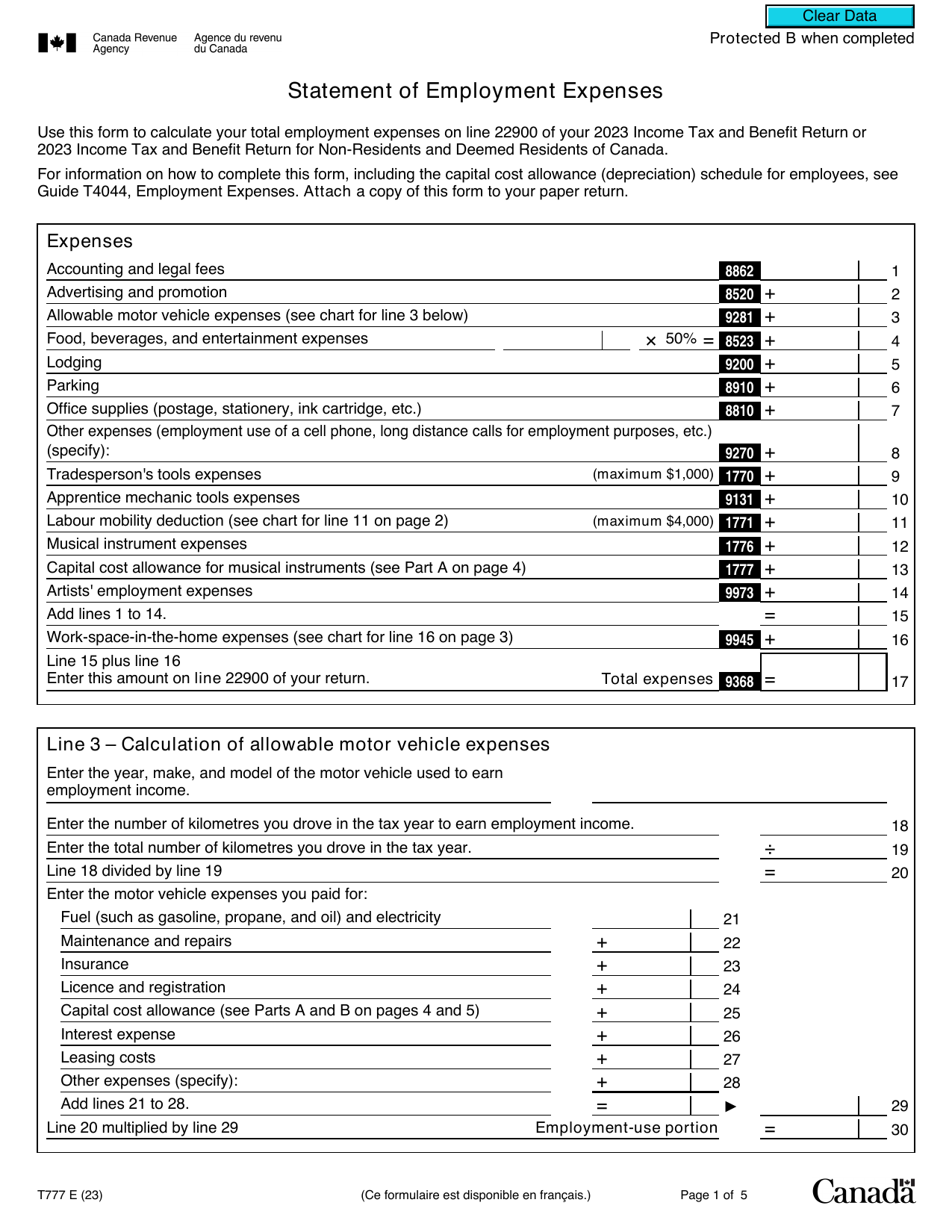

Employees claim eligible vehicle expenses on Form T777.

The CRA requires you to keep a detailed logbook to support any vehicle expense claim. Without it, your deduction can be denied in full during an audit. A compliant logbook must record every business trip and include:

You must also record your odometer reading at the start and end of the calendar year to establish your total annual kilometres driven. Your business-use percentage is calculated as:

Business-use % = Business kilometres ÷ Total kilometres × 100

If you kept a full logbook for a previous year and your business use has not changed by more than 10%, you may be eligible to use a three-month sample logbook in subsequent years. However, you must keep both the original full logbook and the sample logbook on file. Given how scrutinised vehicle claims can be, many accountants — including the team at Swift Accounting Ltd. Calgary — recommend maintaining a full logbook every year to be safe.

Once you have established your business-use percentage, you can apply it to the following eligible operating expenses:

Personal expenses, traffic fines, and the cost of commuting between home and a regular place of work are never deductible.

If you lease a passenger vehicle, the CRA caps the deductible monthly lease payment. For 2025, the monthly deductible limit is $1,050 (before GST/HST/PST) for non-ZEV passenger vehicles, and $1,625 per month for zero-emission passenger vehicles. Your deduction is the lesser of your actual monthly lease payment or the applicable limit, multiplied by your business-use percentage. Amounts above this threshold are not deductible regardless of your business-use percentage.

The CRA also publishes prescribed per-kilometre rates that employers use to reimburse employees for business driving without triggering a taxable benefit. For 2025, the rates are 72 cents per kilometre for the first 5,000 business kilometres driven in the year, and 66 cents per kilometre for each additional kilometre. If an employer pays a reasonable allowance at or below these rates, the allowance is not taxable to the employee — but the employee cannot also claim vehicle expenses. Self-employed individuals cannot substitute the per-kilometre method for actual expenses; they must track real costs against a compliant logbook.

When you purchase a vehicle for business use, you cannot deduct the full purchase price in the year of purchase. Instead, the CRA requires you to depreciate the vehicle over time using Capital Cost Allowance rules.

The classification of your vehicle determines your CCA rate and whether the $38,000 cost limit applies:

| Class | Applies To | CCA Rate | Cost Limit |

|---|---|---|---|

| Class 10 | Motor vehicles and passenger vehicles costing $38,000 or less (before GST/HST) | 30% | None |

| Class 10.1 | Passenger vehicles costing more than $38,000 (before GST/HST) | 30% | $38,000 maximum |

For Class 10.1, the deductible CCA is calculated on a maximum cost of $38,000 regardless of what you actually paid. Each Class 10.1 vehicle must be tracked in its own separate CCA schedule, and the half-year rule applies in the year of acquisition (you can only claim half the normal CCA in the year you buy the vehicle). One taxpayer-friendly exception applies to Class 10.1: in the year you dispose of the vehicle, you can still claim a half-year of CCA — unlike Class 10, where the normal rules give you nothing in the year of disposal.

Battery electric, plug-in hybrid electric, and hydrogen fuel cell passenger vehicles get a higher luxury threshold than gas-powered vehicles. For 2025, ZEVs costing $61,000 or less generally qualify for accelerated CCA. ZEVs costing more than $61,000 fall into Class 10.1, but with the CCA cost capped at $61,000 instead of $38,000. Class 55 applies specifically to ZEV taxis and rideshare vehicles and carries its own accelerated CCA rate.

Suppose you purchased a passenger vehicle in 2025 for $52,000 and used it 70% for business purposes.

In year 2 (assuming the same 70% business use), the full 30% rate applies to the $31,450 UCC: $31,450 × 30% × 70% = $6,605 deductible.

If your employer provides you with a company vehicle that you are also allowed to use personally, the CRA requires that a taxable benefit be included in your employment income. This benefit has two components:

The standby charge is a taxable benefit for simply having access to an employer-owned or employer-leased vehicle. For an employer-owned vehicle, the standby charge is generally 2% of the original cost of the vehicle per month. For a leased vehicle, it is two-thirds of the monthly lease cost (before GST/HST).

The standby charge can be reduced if personal-use kilometres are less than 1,667 km per month (20,004 km annually) and the vehicle is used primarily for business (more than 50% business use).

In addition to the standby charge, an operating cost benefit of $0.35 per personal-use kilometre applies for 2025. Alternatively, if more than 50% of the vehicle's use is for employment purposes, you can elect to have the operating cost benefit calculated as 50% of the standby charge — whichever is lower. Your employer reports both benefits on your T4 slip, which then appear as employment income on your T1 return.

If you are registered for GST/HST (required once your taxable revenues exceed $30,000 in a calendar quarter or over four consecutive quarters), you may be able to claim Input Tax Credits (ITCs) on the GST/HST paid for business-use vehicle expenses. The ITC is calculated based on the same business-use percentage used for your income tax deduction. Keep all receipts showing GST/HST amounts paid. For passenger vehicles in Class 10.1, the ITC on purchase is limited to the GST/HST on the $38,000 cost cap.

The CRA requires you to keep all vehicle expense records — logbooks, receipts, and insurance documents — for a minimum of six years from the end of the tax year to which they relate. Digital records are acceptable provided they are legible and complete. Many clients of Swift Accounting Ltd. use cloud-based mileage tracking apps such as MileIQ or TripLog to automatically generate CRA-compliant logbooks, reducing the administrative burden significantly.

In theory, yes — if your vehicle is used exclusively for business and you have the logbook to prove it, you can deduct 100% of eligible operating costs and CCA. However, the CRA scrutinises high business-use percentages closely, especially when a single vehicle is claimed at 100%. If the vehicle is truly personal-use-free (for example, you have a separate personal vehicle), ensure your logbook clearly reflects this. Home-to-work commuting is never considered business use, even for self-employed individuals whose home is their primary office, unless they are travelling to a different work site.

A passenger vehicle is defined by the CRA as a motor vehicle designed or adapted primarily to carry individuals on a highway and seating no more than the driver plus eight passengers. Passenger vehicles are subject to the $38,000 Class 10.1 cost limit and the monthly lease deduction cap. A motor vehicle (such as a truck with a cargo area, or a vehicle clearly designed for carrying goods) may fall into Class 10 without the cost cap. The distinction matters significantly for large trucks and SUVs — always confirm the classification with your accountant before filing.

Yes. The CRA requires a separate logbook for each vehicle you are claiming business expenses on. If you use two vehicles interchangeably for business — for example, a personal car and a work van — each must have its own complete logbook tracking total and business kilometres for the year.

No. Vehicle expense deductions apply only to vehicles you own or lease. Rideshare fares paid for business travel are deductible as a travel expense (not a vehicle expense), and you should retain the receipts or digital records to support the claim. These are claimed under "Other expenses" on Form T2125 for self-employed individuals, or may be included in employment expenses for qualifying employees.

Vehicle expense deductions are among the most audit-prone claims on a Canadian tax return, but they are also genuinely valuable when claimed correctly. Getting your logbook right, understanding the Class 10.1 cost cap, and applying the right business-use percentage are the keys to maximising your deduction while staying fully compliant with CRA rules. Use our Vehicle Expenses Calculator to estimate your deductible operating costs and CCA before you file. If you are unsure whether your vehicle qualifies, need help setting up a proper tracking system, or want a professional review of your vehicle expense claims before you file, contact our team today — we are here to help you keep more of what you earn.