Post-secondary education in Canada is a significant financial investment, and the federal tuition tax credit helps ease that burden by converting a portion of your eligible tuition fees directly into a tax reduction. Whether you are a student filing your first return, a parent helping to fund a child's degree, or a recent graduate carrying forward unused credits from past years, understanding how this credit works in 2025 can put real money back in your pocket.

The federal tuition tax credit is a non-refundable credit calculated at 15% of eligible tuition fees paid to a qualifying Canadian educational institution during the tax year. Because it is non-refundable, it can reduce your federal income tax payable to zero — but it cannot create a refund on its own. The good news is that any unused portion does not disappear; it carries forward indefinitely or can be transferred to a supporting family member.

Several provinces and territories also offer a provincial tuition tax credit, each with its own rate and rules. When you file through tax software or work with an accountant, both the federal and provincial portions are typically calculated together.

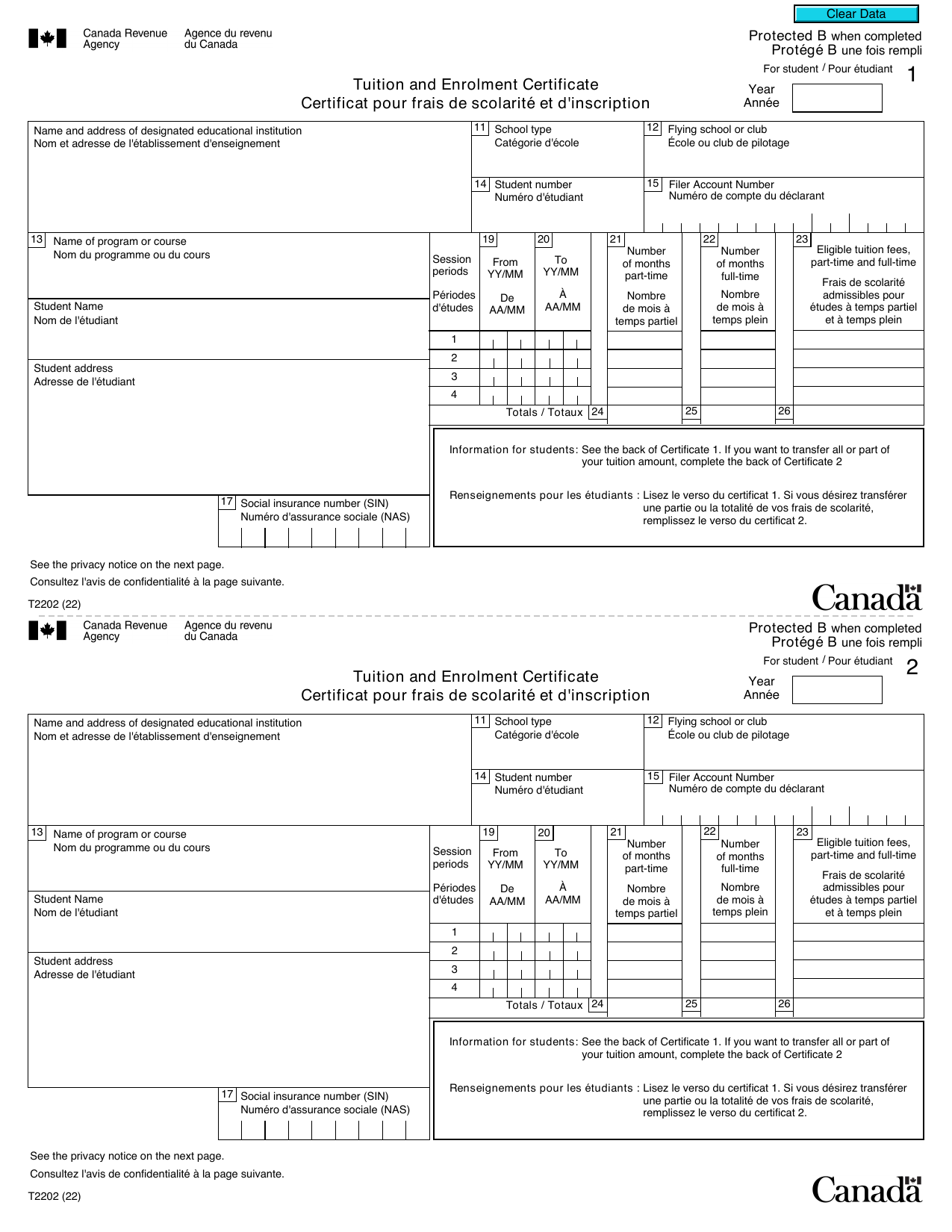

Form T2202 — the Tuition and Enrolment Certificate — is the official document your educational institution issues to confirm the amount of eligible tuition you paid during the calendar year. As of 2019, institutions are required to submit T2202 data directly to the CRA (Canada Revenue Agency) electronically, and students can view and download their certificates through their CRA My Account portal.

Always verify that the amounts on your T2202 match what you actually paid. Discrepancies should be corrected by your institution before you file, as the CRA cross-references T2202 data electronically.

Not every education-related payment qualifies. The CRA considers the following eligible:

The following are not eligible:

The credit is straightforward: multiply your total eligible tuition fees from Box 26 (full-time) and Box 23 (part-time) on your T2202 by 15%.

| Item | Amount (CAD) |

|---|---|

| Eligible tuition fees (T2202) | $12,000 |

| Federal tuition tax credit (15%) | $1,800 |

| Federal basic personal amount credit (15% × $16,129) | $2,419 |

| Federal tax payable before credits | $1,200 |

| Tuition credit applied against tax owing | $1,200 |

| Remaining tuition credit to carry forward or transfer | $600 |

In this scenario, the student reduces their tax to zero and has $600 of unused tuition credit remaining, which they can either carry forward or transfer.

One of the most valuable features of the tuition tax credit is that unused amounts carry forward indefinitely. If you graduate with $4,000 in unused federal tuition credits, you can apply them against your tax in any future year once your income rises and you owe tax.

Many Calgarians who graduated years ago are surprised to discover they have thousands of dollars in tuition credits sitting unused on their CRA account. The team at Swift Accounting Ltd. Calgary regularly helps clients uncover these forgotten balances when reviewing prior-year tax history.

If you have no federal tax payable in the current year and cannot use all of your tuition credit yourself, you may transfer up to $5,000 of the current year's unused federal tuition credit to one of the following:

Note that siblings and other relatives are not eligible to receive a transfer under federal rules.

A student pays $18,000 in tuition and has $2,700 in federal tuition credits. Their own federal tax owing for the year is $300. They apply $300 to eliminate their tax bill, leaving $2,400 in unused current-year credits. They can transfer up to $750 (15% of $5,000) to a parent — but because their remaining unused credit is only $2,400 (15% × $16,000), the transferable portion is capped at the lesser of $750 and the remaining unused amount. The balance beyond the transfer limit becomes a carry-forward in the student's name.

Alberta eliminated its provincial tuition tax credit in 2020, which means Alberta students receive only the federal 15% credit. Students in other provinces — such as Ontario, British Columbia, or Quebec — may still benefit from a provincial credit at varying rates. If you study in one province and live in another, your provincial credit is based on your province of residence on December 31, not where your school is located.

Yes, in limited circumstances. If the foreign university is a recognised degree-granting institution and you were enrolled full-time for at least 13 consecutive weeks in a course leading to a degree, the tuition may qualify. The institution will need to provide documentation equivalent to a T2202. The CRA reviews these claims carefully, so keep all receipts and enrolment records.

Unused tuition carry-forward credits can be applied on the deceased individual's terminal T1 return for the year of death. They cannot be transferred to a spouse or estate after the student's death — they can only be used on that final return.

Yes. Unused tuition credits carry forward indefinitely and do not expire. You can claim them in any future year. If you also believe you missed claiming them on prior returns and overpaid tax as a result, you can request a reassessment for up to ten prior years using a T1-ADJ adjustment request through the CRA. Swift Accounting Ltd. can review your past assessments and file adjustments on your behalf.

Yes. Each tax year, a student may designate up to $5,000 of that year's current eligible tuition fees for transfer. The limit does not accumulate — you cannot transfer $10,000 because the student was enrolled for two years without transferring in the first year. Only current-year fees are transferable, and the $5,000 cap applies annually.

Whether you are a student with a growing carry-forward balance, a parent hoping to benefit from a transfer, or a recent graduate who wants to know exactly what is sitting in your CRA account, the tuition tax credit rules are worth getting right. A missed credit or mishandled transfer can mean leaving hundreds — or even thousands — of dollars unclaimed. If you would like a professional review of your situation, contact Swift Accounting Ltd. today and one of our Calgary-based tax professionals will walk you through your options for the 2025 tax year.