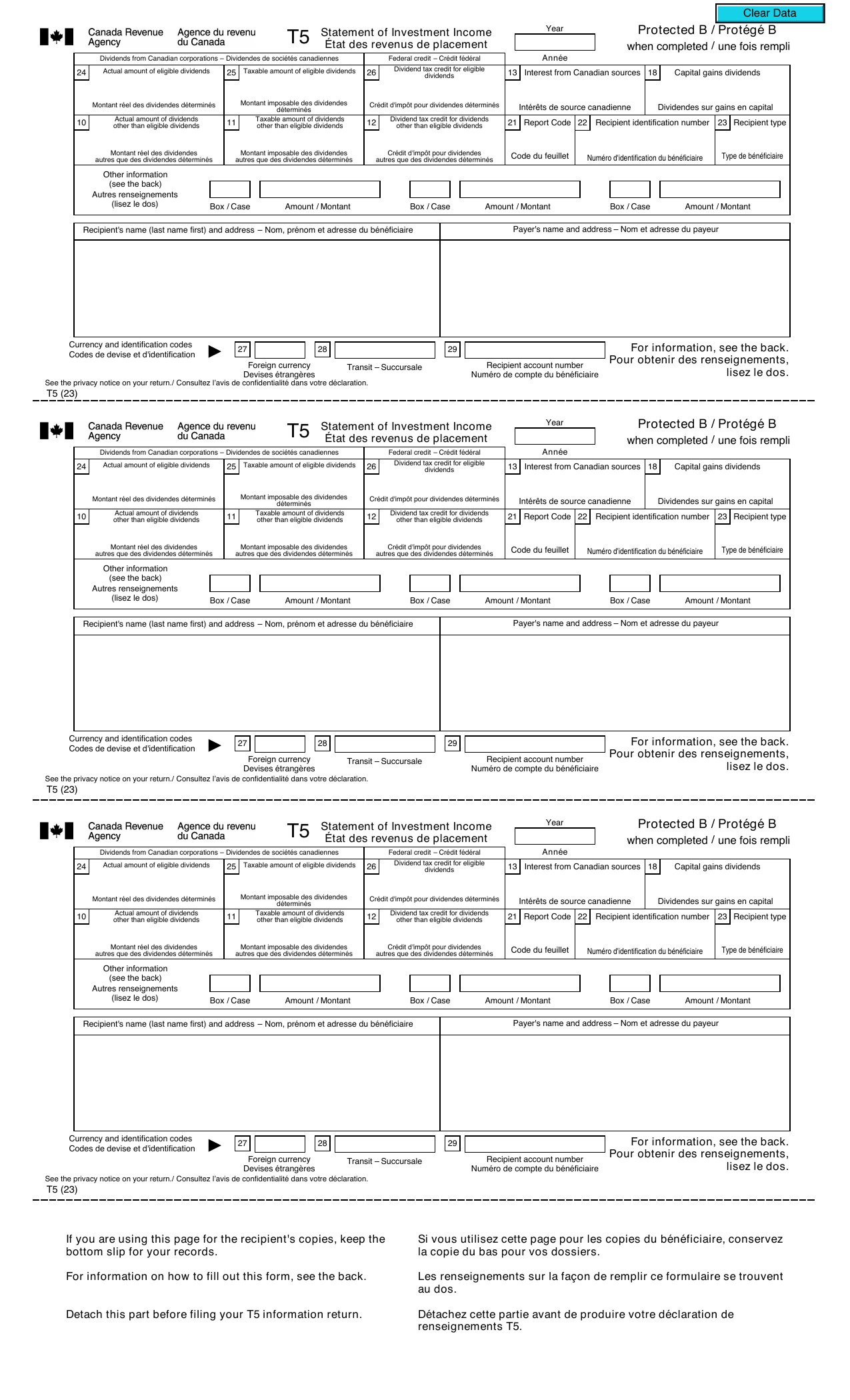

If you received interest from a savings account, dividends from a Canadian corporation, or distributions from a mutual fund in 2024, you likely have a T5 slip waiting for you this tax season. The T5 Statement of Investment Income is one of the most common information slips in Canada, yet many taxpayers are unsure how to read it, where the numbers go on their T1 return, or what happens when a slip never arrives. This guide walks you through everything you need to know about the T5 slip for the 2025 tax filing season — including the correct boxes, tax treatment, and a practical example using 2025 figures.

A T5 slip is an information return that financial institutions, corporations, and other payers issue to report investment income paid to Canadian residents. The Canada Revenue Agency (CRA) requires payers to file a T5 if they pay more than $50 in investment income to a recipient in a calendar year. Both the payer and the CRA receive a copy, and you receive your copy to include with your T1 General tax return.

Common issuers of T5 slips include:

Note that capital gains from selling securities are not reported on a T5 — those appear on a T3 or T5008, or you calculate them yourself on Schedule 3. The T5 covers income earned by your investments, not proceeds from selling them.

Reading a T5 slip is straightforward once you understand the numbered boxes. Here are the boxes you will encounter most often:

Under the Income Tax Act, payers must send T5 slips to recipients by the last day of February following the calendar year in which the income was paid. For the 2024 tax year, that deadline is 28 February 2025. Payers must also file the related T5 Summary with the CRA by the same date.

If you have not received a T5 by mid-March and you believe you should have, contact your financial institution directly. You are still legally required to report the income even if the slip never arrives — you can estimate the amount from your statements and attach a note to your return, or call the CRA at 1-800-959-8281 to request that the slip be re-issued.

Once you have your T5 in hand, reporting is straightforward. Here is where each type of income lands on your T1 General:

If you hold investments jointly — for example, a joint savings account with a spouse — the income must be split proportionally according to who contributed the funds, not necessarily 50/50. Document your contribution ratio in case the CRA asks.

Income earned inside a TFSA is never reported on a T5 — it is completely tax-free. For 2025, the TFSA annual contribution limit is $7,000, bringing the cumulative lifetime limit to $95,000 for a person who has been eligible since 2009.

Income earned inside an RRSP is also not reported on a T5 while it remains in the plan. You only report RRSP income when you make a withdrawal, at which point you receive a T4RSP instead. The 2025 RRSP contribution limit is $32,490. Maximising your RRSP before the 1 March 2025 deadline and sheltering dividend- and interest-paying assets inside registered accounts is one of the most straightforward ways to reduce the tax drag on your investment portfolio.

Suppose Sandra lives in Alberta and received the following T5 income for the 2024 tax year, reported on slips issued in February 2025:

Sandra's total investment income included in her T1 is $1,200 + $4,140 + $575 = $5,915. Assuming her other income puts her in the 26% federal bracket, the $1,200 in interest costs her roughly $312 in federal tax. The eligible dividend gross-up of $1,140 looks alarming, but the corresponding dividend tax credit of approximately $621 (15.0198% × $4,140) substantially offsets the liability, resulting in a much lower effective rate on those dividends. Eligible dividends are generally the most tax-efficient form of Canadian investment income for most taxpayers — often taxed at a lower effective rate than capital gains once provincial credits are factored in.

The federal basic personal amount for 2025 is $16,129, meaning the first $16,129 of Sandra's net income is sheltered from federal tax entirely. Any unused basic personal amount credit can reduce tax on her investment income if her employment income does not already consume it.

A T5 only covers Canadian-source investment income. If you hold U.S. or international stocks, dividends from those positions will typically appear on a T3 (if held in a Canadian fund) or be self-reported on Line 12100 based on your brokerage statements, converted to CAD using the Bank of Canada exchange rate for the date of receipt. Foreign tax withheld — for example, the standard 15% U.S. withholding on dividends from U.S. equities — is claimed as a foreign tax credit on Form T2209 to avoid double taxation.

Yes. The $50 threshold only determines whether the payer is required to issue a T5 slip. You are required to report all investment income on your T1 regardless of amount. If no T5 was issued, use your year-end account statement to determine the correct figure and report it on the appropriate line.

No. Investment income earned within a TFSA or RRSP is sheltered from tax while inside the plan, and no T5 is issued for that income. A T5 is only generated on income earned in a non-registered (taxable) account. Be aware, however, that overcontributing to a TFSA triggers a 1% per month penalty tax, so tracking your cumulative room against the $95,000 lifetime limit is important.

In most cases, the T5 is correct — financial institutions apply specific tax rules when calculating reportable amounts that may differ slightly from the interest credited on your statement. If there is a material discrepancy, contact your bank for a reconciliation before filing. If you have already filed and discover the T5 was incorrect, the institution can file an amended T5; you can then file a T1 adjustment (T1-ADJ) with the CRA.

Yes. Payers send copies of all T5 slips directly to the CRA at the same time they send yours. The CRA's matching program cross-references slips against filed returns and will generate an assessment or request for information if income appears to be missing. Unreported investment income also attracts a repeated failure to report income penalty of 10% of the omitted amount if the same type of income was missed in either of the two preceding years.

Investment income reporting becomes more complex as your portfolio grows — especially when you hold a mix of Canadian dividends, foreign equities, mutual funds, and fixed-income instruments across registered and non-registered accounts. The team at Swift Accounting Ltd. in Calgary works with individual investors and business owners across Canada to ensure every T5, T3, and T5008 slip is captured accurately, the correct credits are claimed, and your overall tax position is optimised for the year ahead. Whether you have a straightforward GIC interest slip or a multi-account portfolio with foreign holdings, we are here to help. Contact us today to book a tax review for the 2025 filing season.